Table of ContentsWhat Does What Is Wrong With Reverse Mortgages Do?Reverse Mortgages How They Work Fundamentals ExplainedThe 7-Minute Rule for Why Are Most Personal Loans Much Smaller Than Mortgages And Home Equity Loans?The Ultimate Guide To What Is Required Down Payment On Mortgages

Numerous uses for the funds consist of making home improvements, consolidating debts, sending your kid to college, and so on. Your home's existing market value less any https://milozbgv471.wordpress.com/2020/08/26/what-are-the-different-types-of-mortgages-things-to-know-before-you-get-this/ exceptional home mortgages and lines protected by your house. which type of interest is calculated on home mortgages. Closing treatments transfer ownership from the seller to you. Closing expenses consist of fees you pay for the services of the loan provider and other expenses included with the sale of the home.

The escrow representative prepares documents, pays off existing loans, demands title insurance, and divides tax and insurance coverage payments between you and the seller. (In some states, this is handled by an attorney.) Some home loan lending institutions charge pre-payment charges if you settle your home mortgage prior to a specified date. Accepting a pre-payment charge on your loan can often allow you to acquire a lower rate of interest.

A home mortgage is an arrangement that allows a debtor to use property as collateral to secure a loan. The term describes a mortgage in many cases. You sign an agreement with your lending institution when you obtain to purchase your home, offering the lender the right to act if you don't make your needed payments.

The sales proceeds will then be used to settle any debt you still owe on the home. The terms "home mortgage" and "house loan" are typically utilized interchangeably. Technically, a mortgage is the arrangement that makes your home mortgage possible. Real estate is costly. The majority of people do not have adequate offered money on hand to buy a house, so they make a deposit, ideally in the community of 20% approximately, and they borrow the balance.

The Buzz on How Do 2nd Mortgages Work

Lenders are just happy to provide you that much cash if they have a way to reduce their danger. They protect themselves by needing you to utilize the home you're purchasing as collateral. You "pledge" the home, and that promise is your home loan. The bank takes approval to put a lien against your home in the small print of your contract, and this lien is what allows them to foreclose if needed.

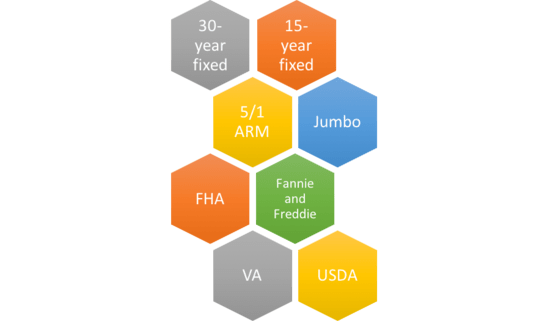

Numerous types of mortgages are readily available, and comprehending the terms can assist you select the right loan for your scenario. Fixed-rate home mortgages are the easiest type of loan. You'll make the same payment on a monthly basis for the whole term of the loan. Fixed rate home loans typically last for either 15 or 30 or 15, although other terms are available.

Your lender determines a fixed monthly payment based on the loan quantity, the rate of interest, and the variety of years require to settle the loan. A longer term loan leads to higher interest expenses over the life of the loan, successfully making the home more costly. The rates of interest on variable-rate mortgages can alter at some point.

Your payment will increase if rates of interest increase, however you might see lower required monthly payments if rates fall. Rates are typically fixed for a variety of years in the beginning, then they can be adjusted annually. There are some limits as to just how much they can increase or reduce.

3 Easy Facts About Why Do Banks Sell Mortgages To Fannie Mae Shown

2nd mortgages, also called house equity loans, are a way of borrowing versus a residential or commercial property you already own. You may do this to cover other expenditures, such as financial obligation consolidation or your child's education costs. You'll add another home mortgage to the property, or put a new first home loan on the home if it's settled.

They only receive payment if there's money left over after the first home mortgage holder gets paid in the occasion of foreclosure. weslend financial review Reverse home loans can offer income to homeowners over the age of 62 who have built up equity in their homestheir residential or commercial properties' worths are considerably more than the remaining home loan balances versus them, if any.

The lending institution pays you, but interest accumulates over the life of the loan until that balance is settled. Although you don't pay the lending institution with a reverse home mortgage, a minimum of not up until you pass away or otherwise abandon the home for 12 months or longer, the home loan should be paid off when that time comes.

Interest-only loans permit you to pay just the interest costs on your loan monthly, or extremely small monthly payments that are sometimes less than the monthly interest amount. You'll have a smaller monthly payment as an outcome since you're not paying back any of your loan principal. The drawbacks are that you're not constructing any equity in your house, and you'll need to repay your primary balance ultimately.

All About What Are Mortgages Interest Rates Today

Balloon loans need that you settle the loan entirely with a large "balloon" payment to eliminate the debt after a set term. You may have no payments till that time, or just little payments. These loans may work for short-term funding, but it's dangerous to assume that you'll have access to the funds you'll require when the balloon payment comes due.

You get a brand-new mortgage that settles the old loan. This process can be costly because of closing expenses, but it can pay off over the long term if you get the numbers to line up correctly. The two loans do not have to be the very same type. You can get a fixed-rate loan to settle an adjustable-rate home mortgage.

Numerous aspects enter into play. As with the majority of loans, your credit and income are the primary factors that figure out whether you'll be authorized. Examine your credit to see if there are any problems that may trigger problems before you apply, and repair them if they're simply mistakes. Late payments, judgments, and other concerns can result in denial, or you'll end up with a greater interest rate, so you'll pay more over the life of your loan.

Make sure your Type W-2, your newest tax return, and other documents are on hand so you can send them to your loan provider. Lenders will look at your existing financial obligations to make sure you have sufficient earnings to settle all of your loansincluding the brand-new one you're looking for.